US stock markets tanked in March while emerging markets led by Asian markets have been able to deliver small positive performance. Commodities prices have been a touch weaker: Brent oil price lost 8% in March, copper was more than 2% down. US natural gas and some softs have been in the lead.

Among various country equities Kenya, where a man from Utah is running for a president, took on a lead in March. Argentina, one of the best markets YTD also maintained its lead in March. Another YTD leader Kazakhstan was a touch weaker in March.

Chemical weapons attack is Syria is what's grabbing everyone's attention, and whether or not Putin will give up support of his longtime ally Assad.

On one hand Putin rarely has been spotted giving up his allies. But he is also somewhat famous for compromises or at least pragmatism.

Syria developments somewhat mirror Iraq developments 20 years where after a Halabja chemical attack in Norther Iraq - public opinion of Iraqi leader was badly affected and even Soviet Union somewhat stepped back from universally supporting Saddam Hussein.

The event certainly provides Putin an excuse to secede from support of Assad and negotiate a larger deal with the US re. Syria.

Putin's ties to siloviki however are among the strongest factors that can weigh against compromise. He could also be seen as possibly expanding his agenda of competition with the US with a possibly utility for later election campaign along this path of argument is rumor of Russia more recent support for Taliban in the Afghanistan.

But in a naiive view a compromise is possible and soon and is likely to involve discussion of Russia sanctions and future for Assad.

US dollar (DXY) has been just a touch weaker in March, but is seen as consolidating before some breaking out higher either in a global run from geopolitical risk or investors chasing higher USD returns and moving out from dividend stocks into US bond markets.

Stronger dollar is bad for oil price, for as long as oil trades in US dollars. But that dollar hegemony will likely be changing as more oil is sold in various other currencies as US moves to export more oil.

Asian markets are quite enjoying the weakness in oil price. US markets are seen a notch weaker in the short term on a profit taking spree, but stronger China markets are providing more fuel to emerging markets. That are speculated to be entering a long term bool market again led by China developments.

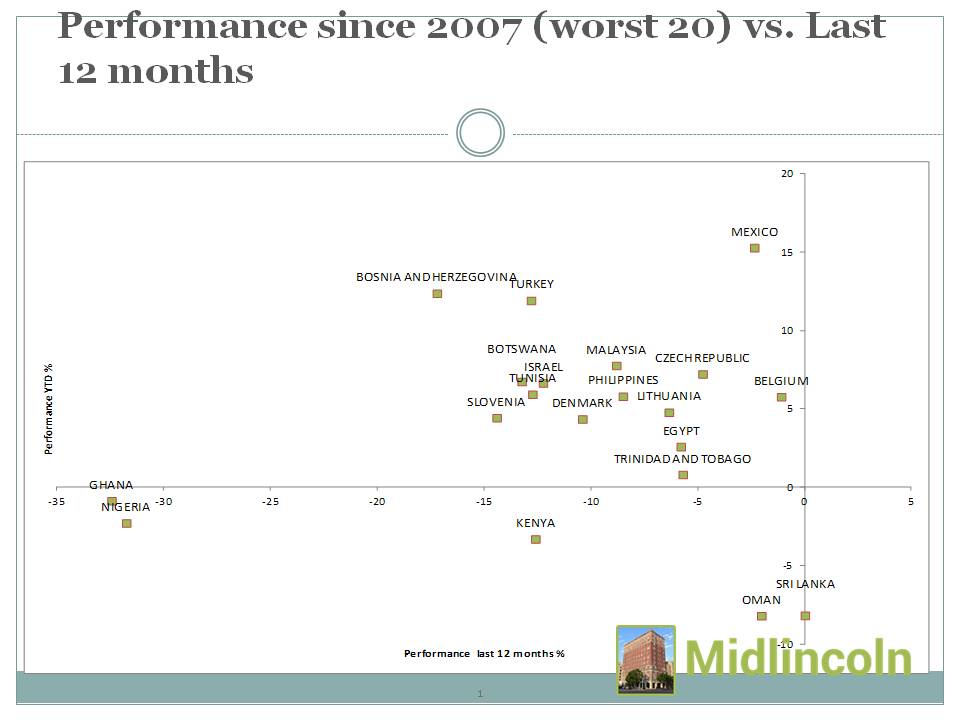

Best last month among various countries' equity markets were KENYA +12.85%, ARGENTINA +10.83%, SPAIN +10.28%, GHANA +9.83%, MEXICO +8.13%, PORTUGAL +7.48%, ITALY +7.38%, CHILE +6.65%, ZIMBABWE +6.54%, NIGERIA +6.34%,

While worst last month among various countries' equity markets were CROATIA -7.29%, OMAN -7.18%, EGYPT -7.12%, MOROCCO -5.64%, NEW ZEALAND -5.46%, PAKISTAN -5.18%, TRINIDAD AND TOBAGO -4.51%, HUNGARY -4.32%, SRI LANKA -4.31%, KUWAIT -4.29%,

Best YTD among various country equities were ARGENTINA +34.79%, KAZAKHSTAN +27.85%, BAHRAIN +17.82%, POLAND +17.75%, JAMAICA +17.05%, INDIA +16.72%, KOREA +16.66%, MEXICO +15.73%, UKRAINE +15.70%, CHILE +15.37%,

While worst YTD among various country equities were OMAN -10.10%, SRI LANKA -7.02%, ZIMBABWE -5.54%, RUSSIA -4.62%, MOROCCO -3.85%, GREECE -3.59%, TRINIDAD AND TOBAGO -3.25%, PAKISTAN -3.01%, NIGERIA -2.45%, SAUDI ARABIA DOMESTIC -2.45%,

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}